The Finatical

Week of April 19th, 2022 - Lifestyle Inflation, Biden's Influence on Asset Management, Use of Bank Data to Spur Business Growth

Topic Breakdown - Lifestyle Inflation

Introduction

Lifestyle inflation is the process of spending more as you are earning more. Basically, as your salary increases, your spending does too. This is also known as “lifestyle creep,” the frequent practice of spending more money as you make more money, becoming accustomed to higher levels of luxury and comfort as your new normal. Lifestyle creep generally occurs following a raise, a new job with a larger salary, or when you repay some of your debt. This is very common and happens to most people, but this can also be considered a problem for some people.

Potential Problems

Let's address the problems with succumbing to lifestyle inflation or lifestyle creep. But first, keep in mind that this is still only a problem if you have a long-term financial goal (which you should definitely consider having). For those who want to enjoy their money in the present and don’t want to worry about their financial situation in the future, lifestyle inflation is not an issue, as it fits their personal goals. Still, it is important to have at least a small plan for your future finances. The problem with lifestyle creep for most people is that whenever a person receives a raise, lifestyle inflation tends to increase, making it difficult to get out of debt, prepare for retirement, or accomplish other long-term financial goals. Lifestyle inflation is often what causes people to become trapped in a cycle of living paycheck to paycheck, with only enough money to cover the expenses each month. In the end, they are not able to save for the future.

Combatting Lifestyle Inflation

Now that we know the problems that come from falling victim to lifestyle inflation, we should learn how to combat it. The first step is being aware of lifestyle inflation and its negative effects, which you have already done by reading this article. Also, many people buy more things just because they can, as they have enough money to do so. Their goal is to buy these items because they make them happy. Instead of making the items, they buy their goal, they should instead try to develop their savings or retirement fund as their goal. One of the easiest ways to combat lifestyle inflation is to set up an automated savings account. The program can automatically save a set amount of your money for you based on your savings goal for the future. This can ensure that along with your spending, you are also saving enough. The best part is that with an automated system, you don’t even have to do anything. Thinking about the “why” behind your purchases is also a key factor in combatting lifestyle inflation. When considering adding a new cost to your life, consider the reasons behind the expense. Lastly, set up a budget. Buying more expensive items is not necessarily a bad thing if it brings you personal satisfaction, but with a budget, you can know how much you should be spending on wants, and how much you should be saving.

In conclusion, the urge for people to spend more as they earn more is known as lifestyle inflation, or lifestyle creep. Lifestyle inflation poses a big risk to your future financial situation, but it can easily be managed. Make sure that as your income increases, along with buying the things you’ve always wanted, also save more money than you did before. Your financial situation in the future is important and is often overlooked.

Financial Trends

Biden's Influence on Asset Management

Mutual fund board directors at asset management companies continue to view the Biden administration’s regulatory and supervisory agenda as a force to bring a transformative change to asset management companies. When the Biden administration came into office, the expectation that asset management companies had with him consisted of making a strong response to the pandemic and making an economic recovery, Through the initial months of Biden’s administration in office, they were able to deal with the promises that it made regarding the pandemic and helping the economy to recover. Asset management companies have witnessed a lot of change in the last decade and there is still more to come. Before the pandemic had commenced, there were already major changes for asset management companies such as tech-driven change and ESG (Environment, Social and corporate governance).

The major changes that asset management companies saw over the past decade consisted of digital transformation, valuation of asset management companies, ESG, and data and privacy. For years, asset management companies have been trying to invest in becoming more digital along with being automated in performing their business operations, streamlining key processes, and enriching the experiences for their customers. Due to the pandemic, the Biden administration had allowed companies to make their employees work from home and the same applies to asset management companies, allowing transformations continuing to expand with data security and setting cyber protections in place. As asset management companies continue to see growth and ongoing changes, the priorities of the Biden administration will continue their pursuit of economic relief and social justice.

Use of Bank Data to Spur Business Growth

It is essential for banks to be the centerpiece of small and medium enterprises (SME) businesses for providing support, capital, and innovative solutions in the pursuit of making small businesses prosper. One of the key factors that help in the growth of the world’s economy is SMEs, as they are sources of innovation and development, and provide the unemployed with jobs. SMEs typically comprise 10 to 2,000 employees and generate annual revenue of 1 million US dollars to 50 million US dollars. Despite these businesses making up a large and diverse group globally across the industry, they face common issues- access to capital, talent, and expertise needed to expand.

SMEs also face a lot of competition from big tech companies and FinTechs. For banks to have control over the industry once again from big tech companies and FinTechs, it is essential for them to use technology for understanding the needs and context of these businesses, allowing them to better serve their customers. The three ways that banks have used data and technology to help these businesses grow to consist of starting neo-banks focused on serving SMEs, partnering up with big techs and FinTechs, and building their own technology. The main objective that banks have from these three methods is to ensure that SMEs are guaranteed to succeed, and FinTechs and big tech companies aren’t able to become a monopoly in the industry. Due to the rate of the competition of FinTechs and big tech companies taking over the industry, banks need to act fast on retaining their SME customers along with entertaining new customers.

Financial Guidance

"The individual investor should act consistently as an investor and not as a speculator." - Ben Graham

As an investor, it’s important to have a rationale and justification for your decisions, rather than basing them on speculations or far-fetched claims.

Money Fact

We’re all used to seeing the familiar faces of famous US figures on our currency. But where did that all begin?

The practice of putting faces on money began with the Romans, who were the first to print the face of various emperors on their coins.

Featured Articles

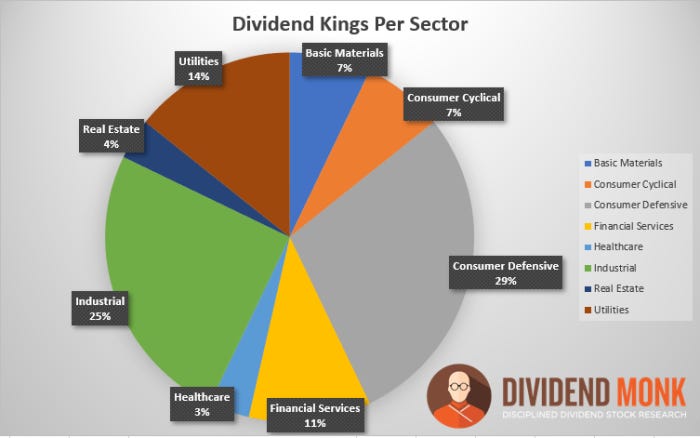

What are Dividend Kings?

The Great Recession

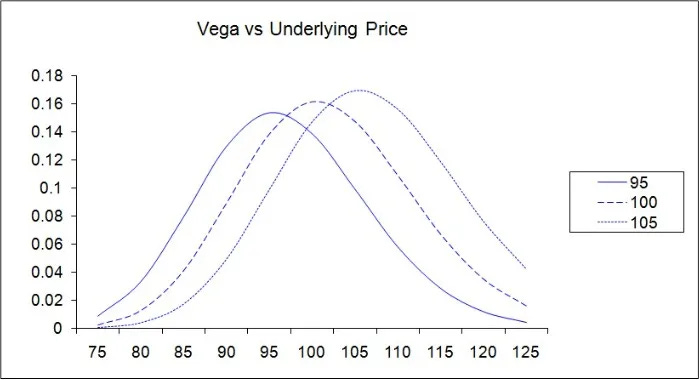

Options Terminology: The Greeks – What is Theta and Vega?

| A guest post by

|

| A guest post by

|

| A guest post by

|