The Finatical

Week of December 6th, 2021 - 401k Tips, Virus Risks in Europe, China's Low Birth Rate

FinaticTips - Learn about a 401(k)

A 401(k) is a defined contribution plan. The employee and employer can make contributions to the account up to the dollar limits set by the Internal Revenue Service (IRS).

A defined contribution plan is an alternative to the traditional pension, known in IRS lingo as a defined-benefit plan. With a pension, the employer is committed to providing a specific amount of money to the employee for life during retirement.

In recent decades, 401(k) plans have become more common, and traditional pensions have become rare as employers shift the responsibility and risk of saving for retirement to their employees.

Employees also are responsible for choosing the specific investments within their 401(k) accounts from a selection their employer offers. Those offerings typically include an assortment of stock and bond mutual funds and target-date funds designed to reduce the risk of investment losses as the employee approaches retirement.

They may also include guaranteed investment contracts (GICs) issued by insurance companies and sometimes the employer's own stock.

Assess Your Risk Tolerance

Risk tolerance is how much loss you can tolerate before you feel the need to sell the investment. Plan managers create 401(k) plans from different types of investments to give you options from which to choose. One of the common problems with these plans is that many people don't know how to decide which types of strategies are best for them. They don't know how their risk tolerance and age can affect their choices.

You can take a few steps to figure out your personal risk tolerance. Begin by completing a risk tolerance questionnaire to get a feel for your level of comfort. Include any concerns you may have about your age. This will guide you in pinning down a risk profile. It will help you find the right investments to include in your profile.

Think about taking advantage of the information sessions and educational resources provided by the financial services firm that manages your 401(k). You can often meet one-on-one and get personalized guidance. It also helps to study on your own. Learn some of the terms so you become more familiar with how a 401(k) works.

Knowing your risk tolerance and a bit about the investment will help you decide how much you want to save.

Avoid Making Withdrawals

The earnings in a 401(k) account are tax-deferred in the case of traditional 401(k)s and tax-free in the case of Roths. When the traditional 401(k) owner makes withdrawals, that money (which has never been taxed) will be taxed as ordinary income. Roth account owners have already paid income tax on the money they contributed to the plan and will owe no tax on their withdrawals as long as they satisfy certain requirements.1

Both traditional and Roth 401(k) owners must be at least age 59½—or meet other criteria spelled out by the IRS, such as being totally and permanently disabled—when they start to make withdrawals.5

Otherwise, they usually will face an additional 10% early-distribution penalty tax on top of any other tax they owe.

Some employers allow employees to take out a loan against their contributions to a 401(k) plan. The employee is essentially borrowing from themselves. If you take out a 401(k) loan, please consider that if you leave the job before the loan is repaid, you'll have to repay it in a lump sum or face the 10% penalty for an early withdrawal. Thus, money withdrawals from your 401(k) plan should be avoided unless it is absolutely necessary.

Roll Your 401(k) Into An IRA

An individual retirement account rollover is a transfer of funds from a retirement account into a traditional IRA or a Roth IRA. This can occur through a direct transfer or by a check, which the custodian of the distributing account writes to the account holder who then deposits it into another IRA account. IRA rollovers can occur from a retirement account such as a 401(k) into an IRA, or as an IRA-to-IRA transfer. Most rollovers occur when people change jobs and wish to move 401(k) or 403(b) assets into an IRA, but some occur when account holders want to switch to an IRA with better benefits or investment choices.

By moving the money into an IRA at a brokerage firm, a mutual fund company, or a bank, the employee can avoid immediate taxes and maintain the account's tax-advantaged status and the employee will be able to choose among a wider range of investment choices than with their employer's plan.

The IRS has relatively strict rules on rollovers and how they need to be accomplished, and running afoul of them is costly. Typically, the financial institution that is in line to receive the money will be more than happy to help with the process and avoid any missteps

FinaticTrends - 2 Financial Trends

1 - Virus Remains a Risk in Europe

The biggest threat to economic recovery in Europe is a sudden surge in infections, principally in northern countries, including Germany, Austria, Slovakia, Czech Republic, the Netherlands, and Belgium. Infection rates remain low in southern countries including France, Italy, Spain, and Portugal. The main difference between these two groups is rates of vaccination, which are higher in the south. Moreover, the northern countries now have colder weather, meaning that people are likely spending more time indoors, thereby making it easier for the virus to be transmitted from person to person.

In the northern countries noted above, infections either match or far exceed the peak rates reached before this winter. However, rates of hospitalization and death remain far below the peak rates. This likely indicates that some of the people becoming infected are vaccinated and, therefore, less prone to sickness. It might also be due to a younger mix of people getting infected who are less likely to get sick.

In any event, governments are becoming concerned, both from a public health and economic perspective. The government of Austria announced that it will seek legislation to make vaccination mandatory from February 1. This move is already highly contentious. In addition, the government will initiate a strict lockdown for the next three weeks. After the lockdown is lifted, unvaccinated people will be restricted in where they can go. Let’s see how all of these changes affect the global economic outlook over the next few weeks.

2 - China’s Low Birth Rate

China has a large population of more than 1.4 billion people—yet that might not be enough. There was a time when China’s leaders worried about too many people and imposed restrictions on the number of children that couples could have. That is no longer the case anymore. Now, leaders are worried that, with a low birth rate, China faces a growing proportion of old population with fewer younger people to support them. The working age population has been shrinking since 2012. The government has eased restrictions on births, but couples continue to have fewer children. In 2016, China recorded 17.9 million births. By 2020, that number had fallen to 12 million, the lowest since 1961 when births fell sharply due to the famine caused by the Great Leap Forward. As recently as 1987 there had been 25.5 million births.

If births remain low, China’s overall population will soon start to decline. The government has taken steps to encourage people to have more children. Even if this works, the impact on the labor force won’t be felt for another 20 years. Meanwhile, a declining labor force means that, all other things being equal, economic growth will decelerate further. Aside from boosting births, there are a few other things that could be done to address the problem. These include more immigration, having people retire later in life, encouraging more women to join the labor force, and investing more in labor-saving and labor-augmenting technology in order to accelerate productivity growth.

It is popularly known that China is one of the most crucial links in the global supply chain and the deficit of labour and workforce is most likely going to have a major impact globally.

Financial Guidance

"The four most dangerous words in investing are: 'this time it's different." - Sir John Templeton

Follow market trends and history. Don't speculate that this particular time wiill be any different.

Money Fact

$2 bills are not as unique as you think. There are more than 1.1 billion of them in circulation.

Featured Articles

Should Higher Education Be Free

Giffen, Veblen, and Other Types of Goods

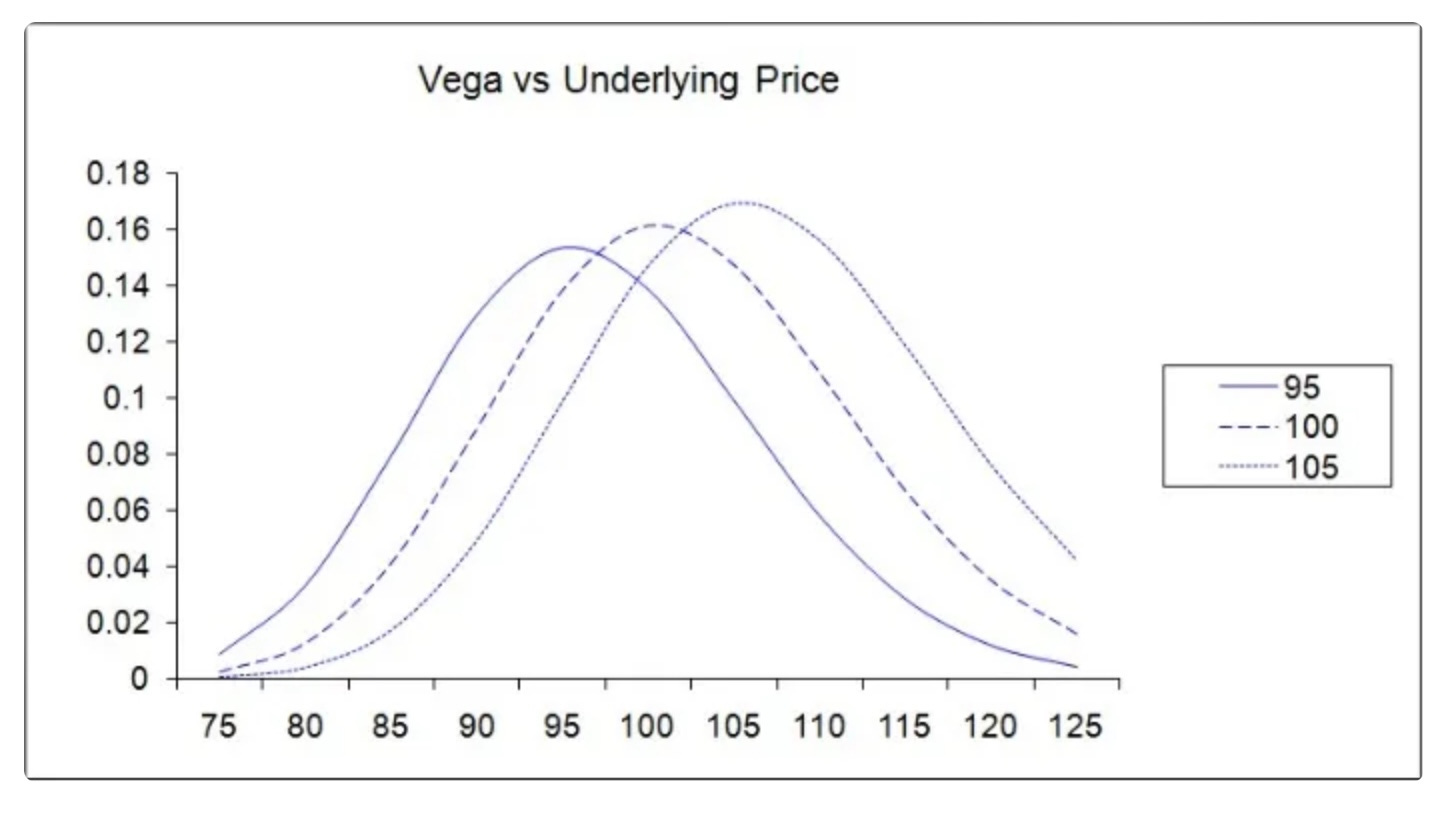

Options Terminology: The Greeks – What is Theta and Vega?

|

|